April 12, 2021

Blog - All about loading in one place

Quo vadis, e-commerce?

E-commerce has been identified for several years as one of the most important trends in supply chain development. No one could have predicted that this process would become the leading investment made by companies in almost every sector. Enormous expenditure is made at the so-called “last mile” stages, which is perfectly illustrated by the recent activities of InPost, Amazon or Aliexpress. E-commerce, however, is a much broader issue.

How much are we able to automate the process of completing online shopping over the next few years? We asked 3 experts in their fields for an opinion.

7 out of 10 Internet users did online shopping in 2020

The litmus test of global e-commerce growth is still the United States, where most online purchases are made. According to a report by the Digital Commerce 360 organization, the year 2020, in relation to the previous one, brought an increase in profits from online sales by… 44%. By comparison, a technologically and logistically developed country like Poland achieved an increase of 30%, the highest in Europe. The US-based Amazon has indicated that it saw a 20% increase in website visits in January 2021, compared to January 2020. If we look at February for both years, we already see an increase of 37%. What is Europe missing to achieve such growth? We asked Arkadiusz Kawa, e-commerce expert, director of the Łukasiewicz Institute of Logistics and Warehousing, professor at the Poznań School of Logistics, for his opinion.

“In fact, the Chinese have the largest share of online sales in the world, both by value and by share in total sales. According to eMarketer, e-commerce reached $2.3 trillion in 2020 and constituted around 45% of total sales. In the US it was $0.7 trillion and 14.5% respectively. The 50% barrier in China is expected to be broken this year. This means that Chinese people will buy more online than in traditional shops. Europe made about 0.7 trillion from online sales in 2020, which constituted about 21% of total sales. As we can see from these values, Europeans are not much different from their American colleagues. However, we are very different from the Chinese. Asians have been very quick to break down barriers and have no concerns about selling online. In some areas, they are creating new solutions themselves. China is dominated by telephone purchases using electronic payments. Deliveries in the OOH (out of home) model, i.e. with collection in parcel lockers and PUDO points, are much more developed. Quick delivery and cross-border shopping (cross border e-commerce) are also more popular. Livestream shopping, which started to grow in Europe during the pandemic and closure of stationary shops, is also of great importance.”

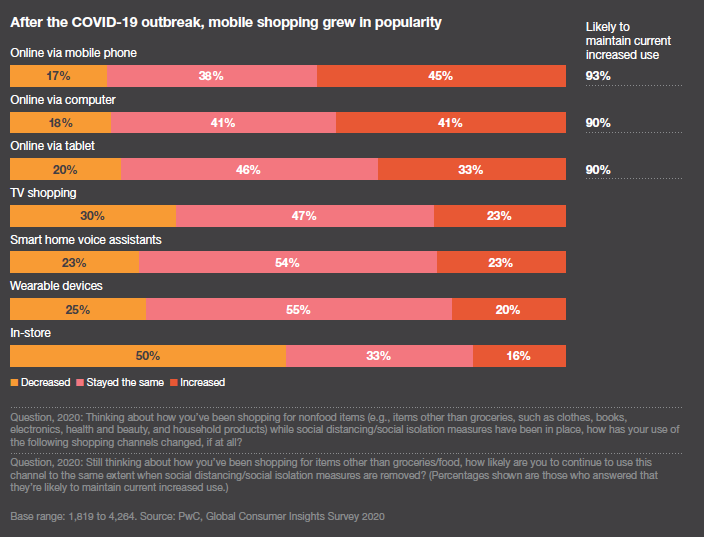

According to the Global Consumer Insights Survey 2020 report by PwC, classic in-store purchases have decreased by 50%, compared to the time before the pandemic, while online purchases made over the phone have increased by 45%. The most popular goods bought online were clothes – 64%, followed by catering services – 29% and home accessories and furniture – 28% (Eurostat data). As producers of the load optimization software, we have noticed an increase in interest in the furniture and KEP industries, particularly after the introduction of the possibility of integration with transportation management systems. What is the situation with e-grocery?

In addition to the trend of mobile shopping, online grocery shopping has increased in popularity during the pandemic. According to the Online Grocery – Global Market Trajectory & Analytics report, due to the COVID-19 crisis, the global online grocery market is expected to reach $550.7 billion in size by 2027, growing by 15.7% between 2020 and 2027.

Business Insider, on the other hand, claims that in the US, despite “only” 2.3% growth in online grocery shopping popularity in 2020, the year 2024 will “serve” 55% of US shoppers.

Last year showed that the increase in demand for grocery purchases outstripped the capacity of suppliers worldwide, which meant that the increase in purchases, although noticeable, was not as spectacular as in other sectors. As people get used to the, no longer so exceptional, situation and the possibility of a return to normality, will there be a further refrain from investment? Refrigerated lockers are still not as popular as the clear expansion of classic parcel lockers in the world, and residents of smaller towns do not have access to such a service at all. Is this a result of low profitability?

Arkadiusz Kawa: “The popularity of e-grocery depends on the region. In countries such as the US and Singapore, the market was growing rapidly well before the pandemic. In Poland it was different. The share of e-grocery in e-commerce has been unchanged for the last few years at around 2.4% of total e-commerce, indicating an equal growth in relation to total e-commerce. In 2019, only around 0.8% of FMCG was bought online. Last year, e-grocery clearly gained momentum. E-grocery grew much faster than other industries and increased its share to 2.7% in total e-commerce and to around 1.1% in total FMCG sales, reaching around PLN 2.1 billion in turnover. For comparison, in 2017 the market was just over PLN 1 billion. The relatively slow development of the Polish market in recent years compared to its Western counterparts was mainly due to the relatively low popularity of this form of shopping and a limited number of sellers delivering products on the same day. The development of e-grocery was affected by the problems of companies that were pioneers in Poland in selling groceries on the Internet. First, the Alma chain went bankrupt, then Tesco began to withdraw from many Polish cities, and then there were the problems of Piotr and Paweł, which seemed to be the future leader in e-grocery. The profitability of this business is, therefore, an important issue. Due to the very high competition, companies rely on small margins. In 2019, Lidl also entered e-commerce, but for the time being with the sale of “non-food” products only. What is interesting, Lidl started with “non-food” products and has not introduced online grocery until today. The mentioned refrigerated locker has been developed by InPost for over 5 years. Currently it has about 50 of them. For comparison, since that time InPost has installed about 10 thousand standard parcel lockers. All this shows that e-grocery is a very difficult industry. The dense network of grocery shops does not help in the development of e-grocery either. In Poland, there are over 70,000 shops in which one can buy groceries. They are in close proximity to customers who often prefer walking to the shop immediately when they need specific products. Besides, a quite frequent shopping for groceries is a characteristic feature of Polish customers of stationary shops – on average twice as much as in other EU countries. This is mainly due to lower incomes and lack of space in homes for larger purchases.”

Same-day delivery

Only a few years ago, online shops offered delivery within 3-4 working days. Nowadays this time is much shorter, even 1-2 days, which is expected by about 25% of customers. By getting people used to ever shorter delivery times, it may not be long before more and more people start using the same-day delivery option. At the moment, it is definitely much more expensive than the standard one, but it is one way for online shops to further gain an advantage over stationary ones and, more importantly, it has a strong business justification. A 2018 report by PwC (Global Consumer Insights Survey) shows that up to 41% of consumers are willing to pay more for same-day delivery. On the other hand, The State of Ecommerce Order Fulfillment & Shipping report states that more than 80% of US consumers would prefer same-day delivery, and only 50% of retailers are able to meet this need. Will the KEP sector have enough time to increase its resources in the next 2 years to meet the needs in Poland and Europe? We asked Mr Mirosław Gral, last mile expert, for his analysis:

“Until 2020, the KEP/CEP sector was fairly predictable. Many markets presented stable single- or double-digit growth depending on the geography of the business and changes in the mode of operation being foreseeable for experts. However, the pandemic has rendered all forecasts and assumptions obsolete and here, too, we are dealing with a <<new normality>>.

In case of SDD – same-day delivery, demand for this type of service was limited and growth in the segment ranged between 1-4% prior to the pandemic. As a result of many restrictions put in place to limit the spread of the virus, a great number of markets have seen very dynamic growth, as exemplified by the August 2020 study in the US:

If we observe consumer behaviour and the desire to receive purchased goods in the shortest possible time, we can undoubtedly expect further dynamic development of SDD services in the KEP/CEP sector. According to the 2019/20 survey, around 30% of Europeans believe that the availability of instant same-day delivery is a key factor in the successful closing of a shopping cart. Furthermore, nearly 25% say they are willing to pay an extra charge for urgent delivery. Its popularity will be further driven by the ‘exploding’ e-grocery sector, the wide range of diet catering and restaurant meals with home delivery.”

And how do carriers and couriers react to the new reality?

Mirosław Gral: “The big market players, global courier companies, continue to focus on typical solutions for domestic or international shipments handled in standards of D+1 (next-day delivery) or several days, depending on the type of service and the distance the shipment has to cover. This operating model has been built up over decades and it is difficult to expect global structures to adapt quickly to the same-day delivery model. Operating in this area requires different IT solutions, organization of couriers’ work, distribution warehouses and distribution networks, which entails investment and time. Furthermore, markets differ from one another, which is due to parameters such as wealth of society, culture of a given community, level of technological advancement, etc. Diversity requires a customized approach to the market, which raises the possibility that any attempt to implement a global SDD solution could be a big ‘flop’ on many markets. Hence the approach of companies such as DPDgroup, which has a dedicated solution for SDD services within its structures, yet, it is a separate operational structure called Stuart. It’s a little different for Amazon, where on some markets it offers the SDD service as part of its own Prime network, but at the same time it has a share in Deliveroo, which specializes in servicing this delivery segment.

Thanks to such activities, one organization develops the so-called core business, i.e. domestic and international services, and on some markets it launches a dedicated business to support SDD. There are also local companies that have been operating for years and have adapted their profile to the trend and expectations of the market in the urgent delivery segment. X-press Couriers or CitySprint in the UK could be such an example on our market; both companies are successfully entering into the field of SDD distribution. The third type of business is handling e-grocery and ready meals. In this area, we are seeing a surge in couriers who are expanding their operations to new cities, taking advantage of the situation created by the pandemic and many trade restrictions. Examples of such an activity include local Stava, DeliGoo and global brands such as UberEats or the previously mentioned Deliveroo.

On the whole, operators are prepared for an increase in interest in SDD delivery. Experts estimate that all the KEP, e-commerce and e-grocery sectors will grow thanks to the development of existing companies and new start-ups that invest in the latest technological (IT) solutions supported by artificial (AI) intelligence.

The winners will be those who successfully combine IT with AI, thereby achieving high operational efficiency while contributing to the reduction of emissions. It is an increasingly important aspect of the customer’s purchasing decision and the further development of transport companies’ business.

But that’s a topic for another story.”

Same-day delivery services are already offered by some online shops, such as Amazon. However, they usually apply to larger towns where it is logistically feasible to deliver goods on the same day. The availability of same-day delivery is a standard in western countries. Amazon has already invested a lot in streamlining the shipping process and speeding up deliveries. Today, 50% of Americans have Amazon Prime, a subscription within which they can take advantage of free same-day delivery (in select areas) or standard delivery for free.

Technological and psychological distance reduction

All e-commerce activities are about distance reduction, easy access, simple purchase and quick delivery. Meanwhile, despite the huge interest in shopping, about 70% of Internet users from all over the world abandon their shopping carts. Are they afraid of an unfamiliar payment method or do they like pretend shopping? What needs to happen to increase this conversion? After all, it is thanks to this decision that logistics is investing millions of dollars, euros and yens in e-commerce development. We asked Dawid Sadulski, co-owner of the Ecommerce UX OTREE agency and co-author of the bestselling book: Ecommerce. Simple answers to difficult questions.

“The problem of abandoned carts is not the most important part of the shopping process, but the whole experience, which in Poland is also largely made up of low prices. These prices and the cost of transport determines 60-70% (according to Gemius research) of whether someone will make a purchase or not. Therefore, it can be argued that at a very attractive price, users would be able to put up with all sorts of inconveniences.

The key problem is the lack of trust in e-shops, which caused the average conversion in Poland to be within 1%, where in Western countries it was up to 3% (Great Britain). Surely, COVID will change these parameters.

This problem is noticed by Polish shops, which try to tackle it in various ways. Examples include quality certificates or other image elements designed to inspire trust, which are not popular in Western European countries, while in Poland they are used by up to 86% of shops (Idealo research). The same goes for customer reviews, which have a huge and sometimes decisive influence on purchases right after the price and transport costs.”

Good quality comes at a price

The 21st century, along with technological progress, has brought inversely proportional changes in the longevity of products sold and their quality. This creates a demand for local products (food) or a greater reliance on home-made manufactures (e.g. clothing and furniture). If the pandemic does not result in a severe financial crisis as in 2009, a further increase in the sale of higher-than-standard quality and locally produced products can be expected. These businesses also benefit from e-commerce. For example, Lufa, a Canadian company based in Montreal, has created an online shop for fresh food that they produce themselves. Greenhouses with vegetables are located on the roof of the physical shop, and other products such as eggs and bread are supplied by local producers. Lufa employs several programmers to develop the software. It must consider order collection, warehouse management, customer relations, delivery and payment processing.

In the coming years, will we see a situation in which small businesses are functional enough, like Lufa, to manage the entire process and, at the same time, execute orders on a larger scale? In the age of automation and optimization systems, this is certainly possible.

Obviously, we cannot be sure which consumer behaviours will change and which will remain once the COVID-19 pandemic is over. At this point, however, we can say that technological developments will help logistics in e-commerce to meet the demands of today’s customers, and the coming years will be marked by new processes and solutions that the entire logistics sector should already be looking at.